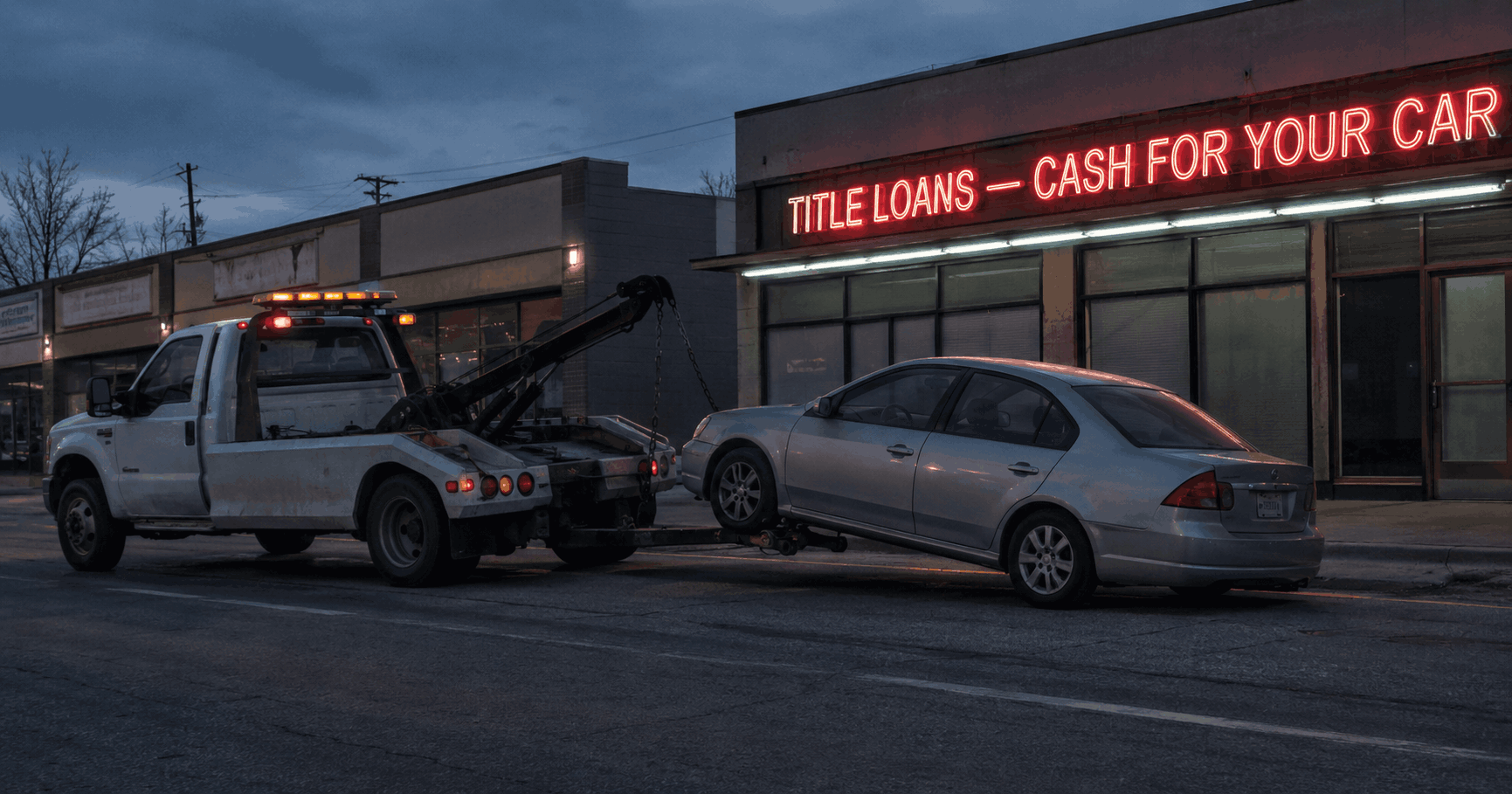

TitleMax is the largest auto-title lender in the United States, operating more than 1,000 storefronts across more than a dozen states. Its offer is simple: hand over your car title, walk out with cash, keep driving. The part the sign leaves out is that your car is the collateral — and the threat of taking it is the leverage the entire business runs on.

This is the second article in our series on vehicle repossession. The first explains how self-help repossession works and what the law requires. This one examines a single lender, because TitleMax’s size and its repeat record with federal regulators make it a clear case study in how repossession harms people — including people who owed nothing.

A note up front: some matters below are pending lawsuits whose allegations have not been proven in court — we label those as allegations, and where a regulator has made a formal finding, we say so. This article is general information, not legal advice.

A title loan carries about 300% interest — and the car is the security

A title loan is a short-term loan secured by your vehicle’s title. You keep the car; the lender records a lien and holds the right to take it if you default.

The Consumer Financial Protection Bureau (CFPB — the federal consumer-finance regulator) found that auto-title loans typically carry an annual percentage rate near 300%. The CFPB also found that one in five auto-title borrowers loses the vehicle to repossession. The loan is structured so a borrower who can’t pay in full rolls the balance over — paying interest, leaving the principal intact, and restarting the clock. The repossession is not a malfunction of that model. It is the model’s backstop.

TitleMax is a repeat offender — by the government’s own findings

These are formal federal findings, not allegations:

- 2016: The CFPB ordered TitleMax’s parent, TMX Finance, to pay a $9 million penalty after finding it misrepresented the true cost of loans to borrowers who renewed them and used illegal, high-pressure debt-collection tactics.

- 2023: The CFPB ordered $10 million in penalties plus more than $5 million in consumer relief after finding TitleMax violated the Military Lending Act by making prohibited loans to military families — often at nearly three times the 36% rate cap that protects servicemembers.

The 2023 action landed while the company was still under the 2016 order. A second federal enforcement action while the first remains in force is the working definition of a repeat offender.

The worst repossessions take cars from people who owe nothing

The most alarming failures aren’t the borrowers who fell behind. They’re the people who owed TitleMax nothing.

In a lawsuit filed in Fresno County, California, Evelyn Jaramillo alleges she was never a TitleMax customer. According to her complaint, she bought a 2004 Toyota Sequoia at a lien sale, paid it off, and held a clean, lien-free California title in her own name. The suit alleges a tow truck working the TitleMax account took the Sequoia at about 3:00 a.m. and did not return it for nearly a month — and that no one checked the title or verified ownership before towing it. (These are allegations; the case’s outcome is not in the public record we reviewed.)

Wrong-car repossessions almost always share one cause: a bad VIN or stale address, a recovery network paid by the car and stretched thin, and no one confirming the title before the hook goes on. Under the non-delegable-duty rule — a lender’s duty to repossess peaceably that it cannot hand off to a contractor — the lender stays liable when the wrong car is taken. This article on the repossession indusrty explains why.

When an agent refuses to stop, repossession turns dangerous

A repossession is supposed to be quiet. The law says the right to self-help repossession ends the moment the owner objects. When agents ignore that line, people get hurt.

Across the industry, agents have towed vehicles with children still inside, lifted occupied cars and kept going after the driver screamed at them to stop, and triggered deadly confrontations after armed police were summoned to a home. Each is a breach of the peace — conduct the law prohibits during self-help repossession. As the post details, even calling the police to push past your objection can itself be the breach.

TitleMax borrowers report the same failures, on the same record

Public complaints to the Better Business Bureau, Trustpilot, and ConsumerAffairs converge on three patterns:

- Borrowers report making a payment arrangement and having the car repossessed anyway.

- Borrowers report cars taken with irreplaceable personal property still inside — documents, IDs, and other belongings they say were never returned.

- Borrowers describe the debt-trap math directly. In one Better Business Bureau complaint, a disabled U.S. Navy veteran reported paying $1,200 to $1,700 a month for 23 months on a $10,000 loan — roughly $22,800 in interest — under what he described as strong-arm tactics and repeated repossession threats.

Three platforms, one story. When complaints converge like that, the problem is the system, not the day.

Your rights if TitleMax repossessed your vehicle

Texas law gives you more rights than the experience makes it feel like:

- A wrongful taking is actionable even if the car comes back. If you were current, had a payment arrangement, or owed nothing, the repossession may have been unlawful — and returning the car later erases neither the violation nor your damages.

- Breach of the peace creates lender liability. Under Texas law (Tex. Bus. & Com. Code § 9.609) and MBank El Paso, N.A. v. Sanchez, 836 S.W.2d 151 (Tex. 1992), a lender is liable for a breach of the peace during repossession — including one committed by an independent contractor, and including when agents refuse to stop or pull police into the dispute.

- Federal law reaches the repo company. The Fair Debt Collection Practices Act (FDCPA — the federal law governing debt collection), at 15 U.S.C. § 1692f(6), bars taking a vehicle when there is no present right to possession — exactly the situation when the wrong car is taken or the loan was paid.

- Your personal property must be returned. Belongings inside the car remain yours.

Recoverable damages can include actual damages (vehicle damage, lost wages, emotional distress), statutory damages under the FDCPA, and in serious cases punitive damages.

They were counting on you not to fight back

A repossession is built to feel final. The car is gone, the morning is ruined, and most people assume there’s nothing left to do but pay up and move on. That assumption is exactly what makes a wrongful repossession so profitable — and it’s wrong.

If TitleMax, or a recovery agent working for it, took your vehicle when you were current, when you had a payment arrangement, when you owed nothing at all, or in a way that put you or your family in danger, the law may be squarely on your side. What that can mean:

- You pay nothing up front. These cases are frequently handled on contingency — no retainer, no hourly bills.

- The lender may have to pay your legal fees. When consumers win FDCPA claims, the lender is often ordered to cover the attorney’s fees on top of your damages.

- You may be owed real money — and your property back. Actual, statutory, and in serious cases punitive damages.

Cases get stronger the sooner they start. A documented payment arrangement or a paid-off title is powerful proof — and it’s easiest to lock down while the records are fresh.

Get your free case review →

Representing consumers in repossession and debt-collection cases across Texas. There is no cost to find out where you stand.

Frequently asked questions

Can TitleMax repossess my car without warning me first?

In most states, self-help repossession doesn’t require advance notice or a court order, as long as the lender doesn’t breach the peace. The lender generally must send notice after the repossession and before selling the car. But if your loan was current or paid off, the taking itself may have been unlawful — notice or no notice.

Can TitleMax repossess my car if I made a payment arrangement?

If the lender agreed to a payment arrangement and then repossessed anyway, that can be a wrongful repossession. Borrowers report this happening, and a documented agreement is strong evidence that the lender had no present right to take the car.

Can they repossess a car I already paid off, or one I never financed with TitleMax?

No. If you owe nothing — because the loan is paid, or because you were never a TitleMax customer — there is no present right to possession, and taking the car can violate both state law and the federal FDCPA (15 U.S.C. § 1692f(6)). Returning the car days or weeks later does not cure the violation.

What happens to my personal belongings inside the car?

Your personal property is still yours, and the repossession company has to give it back. Losing or refusing to return items inside the vehicle — documents, IDs, a child’s car seat, irreplaceable personal effects — can create additional liability for the lender and its agent.

Can a repo agent take my car in the middle of the night?

Time of day by itself usually isn’t illegal. But a nighttime repossession that involves entering a closed garage, cutting a lock, using deception, or refusing to stop after you object can cross the line into a breach of the peace.

Can TitleMax bring the police to repossess my car?

Police are allowed to keep the peace — not to take the car for the lender. If an officer orders you to hand over the keys, tells you to step aside, or threatens to arrest you for objecting, that can turn a private repossession into a breach of the peace and even a constitutional violation. Our hub explains how police involvement crosses the line.

What can I do if my car was wrongfully repossessed?

Save everything — payment records, any arrangement, the date and time it happened, photos, and a list of what was inside the car — and talk to a consumer protection attorney. You may be owed actual damages, statutory damages under the FDCPA, and in serious cases punitive damages, often with the lender required to pay your attorney’s fees.

Think your repossession was wrongful? Don’t let it go unanswered. Get your free case review →