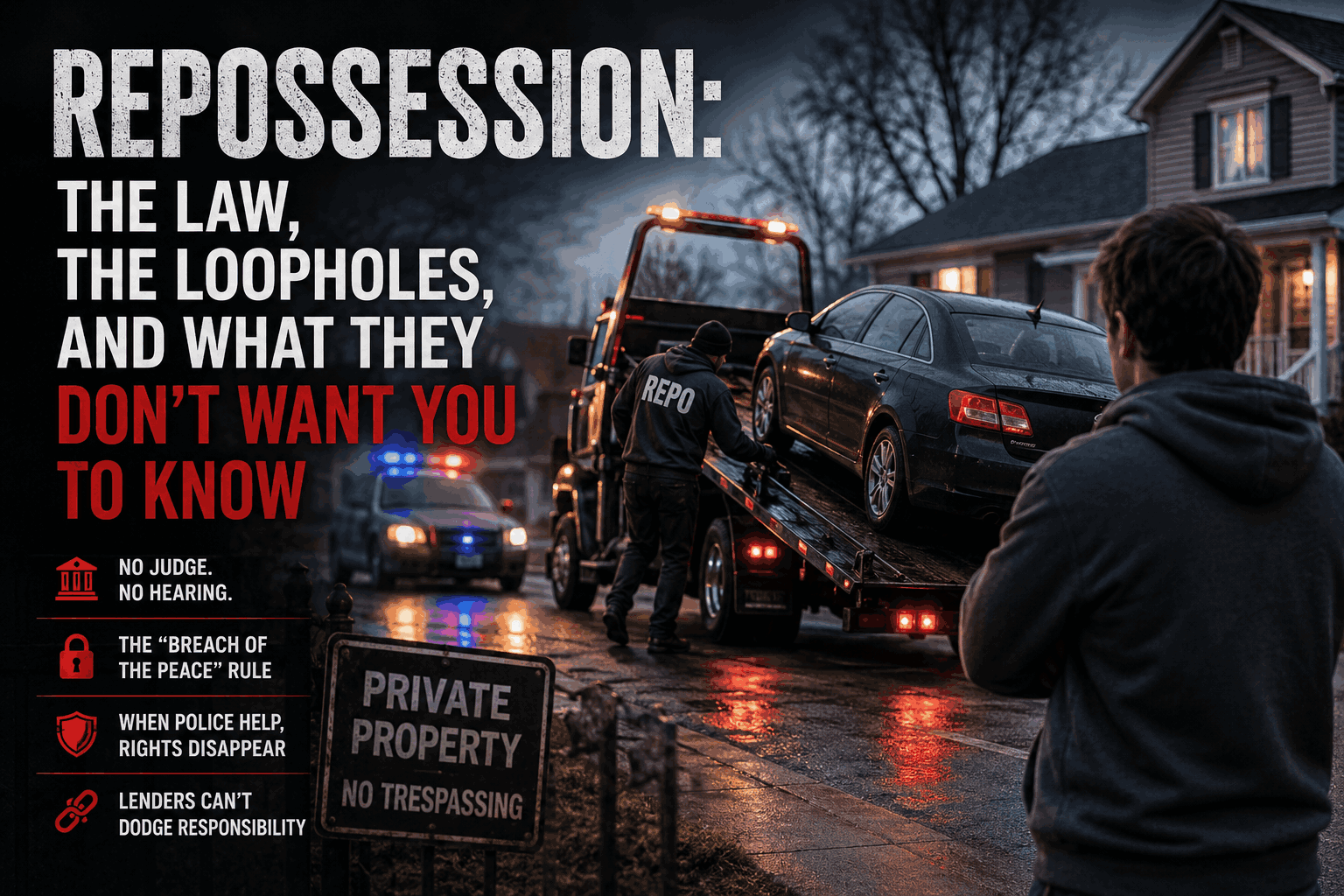

Repossession is one of the only places in American law where a private company can come onto your property and take something you use every day — your car — with no judge, no hearing, and no advance warning. No court signs off first. No officer knocks with a warrant. A company you may have never heard of sends a driver with a tow truck, and if everything goes the way the law allows, the car is gone before you finish your coffee.

That power is real, it is legal, and most people have no idea how it actually works until it happens to them. Understanding the rules matters, because the same system that lets a lender recover a genuinely defaulted loan also, with disturbing regularity, takes the wrong car, takes a car from someone who owes nothing, and turns an ordinary morning into a violent confrontation.

Here is how the machine works, what the law demands of the companies running it, and why the failures are so predictable.

The legal engine: “self-help” repossession

When you finance a vehicle, the lender keeps a security interest in it — a legal stake that lets them take the car back if you stop paying. The rules come from Article 9 of the Uniform Commercial Code, adopted in some form by every state. The key provision is UCC § 9-609.

It gives a secured lender two ways to take the collateral. One is to go to court and get a judge’s order. The other — the one used in the overwhelming majority of cases — is “self-help” repossession: taking the car without any court involvement at all.

There is exactly one condition. The lender may use self-help only if it can do so “without breach of the peace.”

That single phrase is the entire guardrail. And it is doing a lot of work.

What “breach of the peace” actually means

The UCC never defines “breach of the peace.” The drafters left it deliberately undefined and let courts work it out case by case. Over decades, the courts have built a fairly consistent picture of what crosses the line:

- No force or violence. An agent cannot push, grab, or physically intimidate anyone.

- No threats. Threatening a person — or bringing the implied threat of armed authority — can be a breach.

- No breaking in. Entering a closed garage, cutting a lock, or going through a gate to reach the car generally breaches the peace. A car sitting in an open driveway or on a public street is usually fair game; a car behind a closed door usually is not.

- No deception. Tricking someone into handing over the car can be a breach.

- Stop when the owner objects. This is the one most people don’t know and most agents ignore. The moment the person confronts the agent and says stop, the right to self-help repossession ends. The agent is legally required to back off and leave. Pressing forward after a clear objection is the classic breach of the peace.

That last rule is why so many repossessions go wrong. A lawful repo is supposed to be quiet and uneventful. The instant it becomes a dispute — someone runs outside, someone yells stop, someone is still in the car — the law says the agent should walk away. When they don’t, people get hurt.

Calling the police is not a workaround — it can be the breach

One of the most common ways repossessions cross the line is also one of the least understood: the agent calls the police, or asks an officer to come “stand by” while they take the car.

Agents do this because a uniform makes objections disappear. When a squad car pulls up, the owner who would have stepped outside and said stop — and legally ended the repossession — stays inside, because no one argues with the police. That is exactly the problem. Courts have recognized that an officer’s mere arrival alongside the repo agent can give the seizure “a cachet of legality” and intimidate the owner out of exercising the right to object, which facilitates the repossession and breaches the peace. Booker v. City of Atlanta is the leading example of this reasoning.

It gets more serious than a civil breach. A private repo company is not a government actor, so it owes you no constitutional due process. A police officer is. When an officer crosses from neutrally keeping the peace into actively helping — ordering the owner to hand over the keys, telling them to “step aside,” or threatening arrest for objecting — the officer may convert a private repossession into state action, taking your property without the due process the Constitution requires. That can support a federal civil-rights claim under 42 U.S.C. § 1983 on top of the repossession claims.

The line is simple in theory: police may be present to prevent violence, nothing more. They cannot take the keys, cannot order you out of the way, and cannot threaten you for protesting. The moment they do, an agent who couldn’t lawfully take the car alone has used the power of the state to take it anyway. And when armed officers are summoned to a debt dispute at someone’s home, the risk is no longer just a wrongful taking — it is a confrontation that can turn deadly.

The duty the law puts on the lender — and won’t let them dodge

Lenders rarely send their own employees to take cars. They hire repossession companies, who are usually independent contractors. Lenders often assume that hiring a contractor puts a wall between them and whatever that contractor does in your driveway.

It does not. Courts across the country have held that a lender’s duty to repossess peaceably is non-delegable. The lender stays legally responsible for a breach of the peace even when an independent contractor commits it, and even if the lender did nothing wrong itself.

The Texas Supreme Court said it plainly in MBank El Paso, N.A. v. Sanchez, 836 S.W.2d 151 (Tex. 1992): a secured creditor is liable for a breach of the peace committed during repossession, including by an independent contractor. The reasoning is that self-help repossession is inherently risky, and a lender cannot hand that risk to a cheap contractor and wash its hands of the consequences. Some courts add a second theory — negligent selection — holding a lender responsible for carelessly choosing a bad repo agent in the first place.

The practical upshot: when a repossession injures someone or takes the wrong car, the lender is on the hook, not just the tow driver. That is by design. The law puts the duty where the money and the decision-making are.

How the industry is actually built

To understand why repossessions keep going wrong, you have to look at the economics of the business doing them.

The repo industry is shrinking and under strain. Roughly 30% of repossession companies closed permanently during the pandemic. The flat fee an agency earns per car — generally $200 to $500 — has barely moved in decades, even as the cost of tow trucks, insurance, bonding, and compliance climbs. Skilled, licensed, certified agents are leaving the field. And the work is dangerous, which makes hiring and keeping good people harder still.

Meanwhile, the demand has surged. About 1.73 million vehicles were repossessed in 2024, a sharp jump from the years before. Recovery rates have fallen — by some industry measures from roughly 41% before the pandemic to around 31% — meaning most assignments don’t even end in a successful seizure. In rough terms, it takes about three assignments worked for every car actually recovered. This means that 1.73 million repossessions required approximately 5,190,000 attempts.

To bridge the gap, lenders increasingly use the “forwarder” model: instead of vetting and supervising repo agents directly, they hand the work to large management companies that parcel it out across sprawling networks of subcontractors. Each layer adds distance between the lender writing the check and the person hooking the car — and distance is where oversight disappears.

Put those pieces together — a shrinking pool of qualified agents, fees that reward speed over care, and a contracting structure that hides who is actually doing the work — and the failures stop looking like accidents. They look like the predictable output of the system.

Who gets hurt — and it runs both ways

Honesty matters here, because the harm is not one-directional.

Repossession can be dangerous for the undertrained agents who do it. The industry press that compiles these numbers and claims the real totals are likely higher than reported. These are real people getting hurt at work, mostly due to the failures of the model, today’s repo agent is undertrained and overworked.

But the people on the other side of the tow hook get hurt too — and they include people who did nothing wrong:

- People who owed nothing. Cars get taken from owners who never had a loan with the lender, whose accounts were current, or who held clean, lien-free titles — usually because someone typed the wrong VIN or chased the wrong address. A car returned a month later does not undo the violation, the lost work, or the damage.

- Children left in cars. In multiple recent incidents, agents towed away vehicles with children still inside — including cases where a child reportedly fell into the roadway, and where agents allegedly lifted an occupied car and kept going after the mother screamed that her child was inside.

- Confrontations that turn deadly. When an agent refuses to back off, or brings armed police to stand by at someone’s home, an ordinary debt dispute can end with someone dead.

Every one of these is a breach-of-the-peace failure. Every one was preventable. And under the non-delegable-duty rule, the responsibility doesn’t stop with the tow driver — it runs up the chain to the company that sent them.

The pattern behind the harm

Strip away the individual stories and the same root cause appears every time: a lender chose not to vet, train, or supervise the people taking cars in its name.

The standards exist. Repossession has certification programs, licensing regimes in many states, and well-understood rules about what a professional operation does — confirm the title and ownership before towing, verify the car is unoccupied, stop at the first objection, document everything, and return personal property. None of that is exotic. It is the baseline of a careful operation.

The harm happens when a lender, under pressure to recover collateral cheaply from a thin pool of agents, sends whoever is available and looks the other way. The law’s answer is direct: the duty to do it right cannot be delegated away, and when it is ignored, the lender pays.

This is the first in a series examining how specific lenders handle repossession. If your vehicle was taken when you were current, when you owed nothing, or when someone was hurt in the process, you may have a claim under the Fair Debt Collection Practices Act and state law. Contact our office for a consultation.x